Redefining "Merger of Equals" In 2026 (& Beyond)

Reading Time: 7 Minutes

Image created by Superhumxn team.

Cohere shareholders will own 90 percent of the combined company, but Aleph Alpha's will own 10. The press conference called it a partnership between equals. Why?

On April 24, Cohere and Aleph Alpha announced they were combining to form what both companies called a transatlantic AI powerhouse, anchored in Canada and Germany. CEO Aidan Gomez described it as two companies uniting to build a global, independent AI champion. The deal carries the backing of both governments, a $600 million financing commitment from Germany's Schwarz Group, and a combined valuation reported at roughly $20 billion.

According to CorpDev.org's reporting on the transaction structure, Cohere shareholders retain 90 percent ownership of the new company. Aleph Alpha's investors receive the remaining 10 percent. Cohere has more than 500 employees. Aleph Alpha has about 200, according to the Globe and Mail. Gomez stays CEO. Cohere stays Canadian headquartered and owned, in his own words, even though he declined to specify where the rest of the executive team or the combined entity's domicile would sit. Aleph Alpha, for its part, had spent the previous year losing its founder and appointing two new co-CEOs.

The term both companies chose for all of this was "merger." The phrase was "global AI powerhouse." The framing was equal partnership between two nations' sovereign AI ambitions, but the deal represents a larger, better-capitalised company absorbing a smaller one.

Berlin gave its blessing to the merger talks on April 10, two weeks before the deal became public. The transaction had been pre-cleared with political stakeholders well before either company's employees, customers, or the market heard the word "merger."

What can I expect from a subscription?

Real-world strategies for navigating the future of work.

AI AGENTS AT WORK

Everything you need to know about how AI agents are changing teams and ways of working.

SUPERHUMXN IRL

Real insights from investors and operators.

MEMOS ON PEOPLE, CULTURE & AI AT WORK

The latest use cases and strategies for change and transformation.

Transaction

An unusual choice under ordinary circumstances

Cohere was valued at roughly $7 billion as of last September. The combined entity is now valued at approximately $20 billion. Cohere has raised $1.6 billion from investors including Nvidia and AMD. Aleph Alpha has raised about $500 million total, most of it years ago, and Wikipedia's company profile listed its headcount at 51 to 200 employees as of 2024, a range that had barely moved by 2026.

Image Source: Getty

Aidan Gomez speaks onstage during the "The Future of Enterprise AI with Cohere" panel at the HumanX Conference San Franciso 2026 at Moscone Center South on April 09, 2026 in San Francisco, California.

Aleph Alpha's leadership over the previous eighteen months told a different story. Founder Jonas Andrulis, who started the company in 2019 to build Europe's first frontier large language model,left in 2025. In February 2026, two months before the merger announcement, the company appointed Ilhan Scheer as co-CEO alongside Reto Spörri. A dual co-CEO structure at a company of 200 people is an unusual choice under ordinary circumstances. It makes sense when the founder has just departed and the board is attempting to stabilise the organisation rather than scale it.

At Toronto Tech Week, Gomez said he was glad Cohere had turned down a nine-figure acquisition offer, framing any future exit that would move Cohere out of Canada as something that would only happen "if we fail." He has said Cohere is "not for sale." Not quite the declaration of shared governance you’d expect.CorpDev.org describes the transaction as "structured as an acquisition where Cohere shareholders will retain 90% ownership. "Tracxn lists Aleph Alpha among Cohere's acquisitions. Wikipedia's entry on Cohere describes it the same way. Hightechinvesting's analysis agrees.

Dual motives

Why “merge”?

There are two competing motives here.

For Germany, backing an outright sale of the country's most prominent frontier AI lab to a foreign buyer is a better story than backing its national AI champion in a strategic transatlantic partnership. The Schwarz Group's $600 million commitment, structured as an investment into Cohere's upcoming Series E rather than as proceeds from selling Aleph Alpha, reinforces that framing. German capital flows into the new combined entity rather than German assets simply being purchased.

Canada and Germany launched theSovereign Technology Alliance at the Munich Security Conference on February 14, 2026, specifically to reduce strategic technology dependencies and build sovereign AI capabilities. Canada's Digital Minister Evan Solomon and Germany's Digital Minister Karsten Wildberger both attended the Berlin announcement on April 24, ten weeks later. The Alliance gave both governments a ready framework to describe the deal in.

For Canada, theGlobe and Mail described Cohere as "crucially important for Canada's AI ambitions," with Ottawa having committed up to $240 million for Cohere to train AI models domestically. A Canadian company quietly absorbing a struggling German lab is one outcome. A Canadian company leading a transatlantic alliance that counterbalances American technology giants is a far more useful story for a federal government building a domestic AI sovereignty narrative.

Gomez described the deal as unlocking "massive scale, robust infrastructure, and world-class research and development talent," language that emphasises capability gained rather than ownership transferred. Nick Frosst, Cohere's co-founder, posted his own framing the day of the announcement, describing the union as putting control of AI back in the hands of those who use it. Both argued sovereignty was the main justification.

The role of "Sovereign AI"

Sovereign AI refers to systems where data residency, model provenance, and operational control are contractually bound to a specific jurisdiction. This matters for regulated industries, public sector buyers, and enterprises operating under the EU AI Act. Schwarz Group's STACKIT cloud platform, which will serve as infrastructure for the combined entity's European operations, is a physical answer to that requirement. The company is reportedly building an €11 billion data centre facility in Germany due for completion by the end of 2027.

Image Source: Data Center Dynamics

Schwarz Group's STACKIT infrastructure lies behind the sovereignty claim.

"Sovereign AI" lets a 90/10 acquisition be described as a defence of national capability. It lets Aleph Alpha's German backers describe a company that lost its founder and brought in emergency co-leadership as contributing "European R&D excellence" to a powerhouse. It lets Cohere expand its scale and European market access as a service to customers who need data sovereignty, rather than as growth by purchase.

The data residency requirements are genuine, and the EU AI Act's enforcement mechanisms are real. Regulated European enterprises do want AI infrastructure they can guarantee stays within certain jurisdictions. None of that changes the ownership structure.

Case

Although the ownership structure seems misleading, the product fit works.

Cohere has built its business around large language models for regulated industries, with customers including Royal Bank of Canada, BCE, Fujitsu, and LG CNS. Aleph Alpha had already pivoted away from competing in frontier model development toward an AI deployment and integration layer, with its PhariaAI platform serving Deutsche Bank, Bosch, and SAP. Gomez has pointed to Aleph Alpha's focus on small language models, European languages, and tokenisers as complementary to Cohere's broader focus on large language models, and that assessment appears accurate.

Cohere gains a foothold in Germany's industrial base, specifically customers that are among the most conservative, security-conscious buyers in Europe and that take years to win from scratch. Aleph Alpha's investors get liquidity and access to a larger parent company at a moment when the smaller company's path to profitability had become uncertain enough to require new leadership. A unified Command-Pharia 1 model is planned for Q4 2026, which is the clearest evidence that the product integration is being taken seriously rather than left as an aspiration.

One relationship worth watching specifically is SAP, which appears on both sides of the deal, as an investor in Aleph Alpha and a named customer of Cohere. That overlap validates the shared positioning, but it also means the combined entity will need to manage a partner relationship that sits across two previously separate commercial relationships. A 90/10 split with product fit is a sensible acquisition. The press conference described something else entirely.

There is also a structural risk built into Gomez's own promise that "Cohere will become a Canadian-German company. "TechCrunch noted that if Cohere goes public, ownership passes into the hands of global shareholders, and the guarantee of Canadian-German control becomes much harder to keep. The IPO timeline is not confirmed, but Cohere had been reported as exploring it before this deal was announced.

Image Source: Cohere Platform Dashboard

Mistral

Analysts suggest a capital raise

The combined Cohere-Aleph Alpha entity's $20 billion valuation moves France's Mistral AI, previously Europe's most valuable AI lab at a $13.7 billion valuation, into second place.

That is not incidental to the timing. European AI had exactly one company most observers pointed to as a credible homegrown alternative to the American labs. A deal that instantly creates a larger, better-funded competitor repositions the entire European AI conversation in ways that benefit both Cohere and the German government, independent of whatever happens with Aleph Alpha's technology or remaining team. Analysts covering the deal have suggested Mistral will need to respond with a major capital raise, a new strategic partnership, or both before the end of 2026.

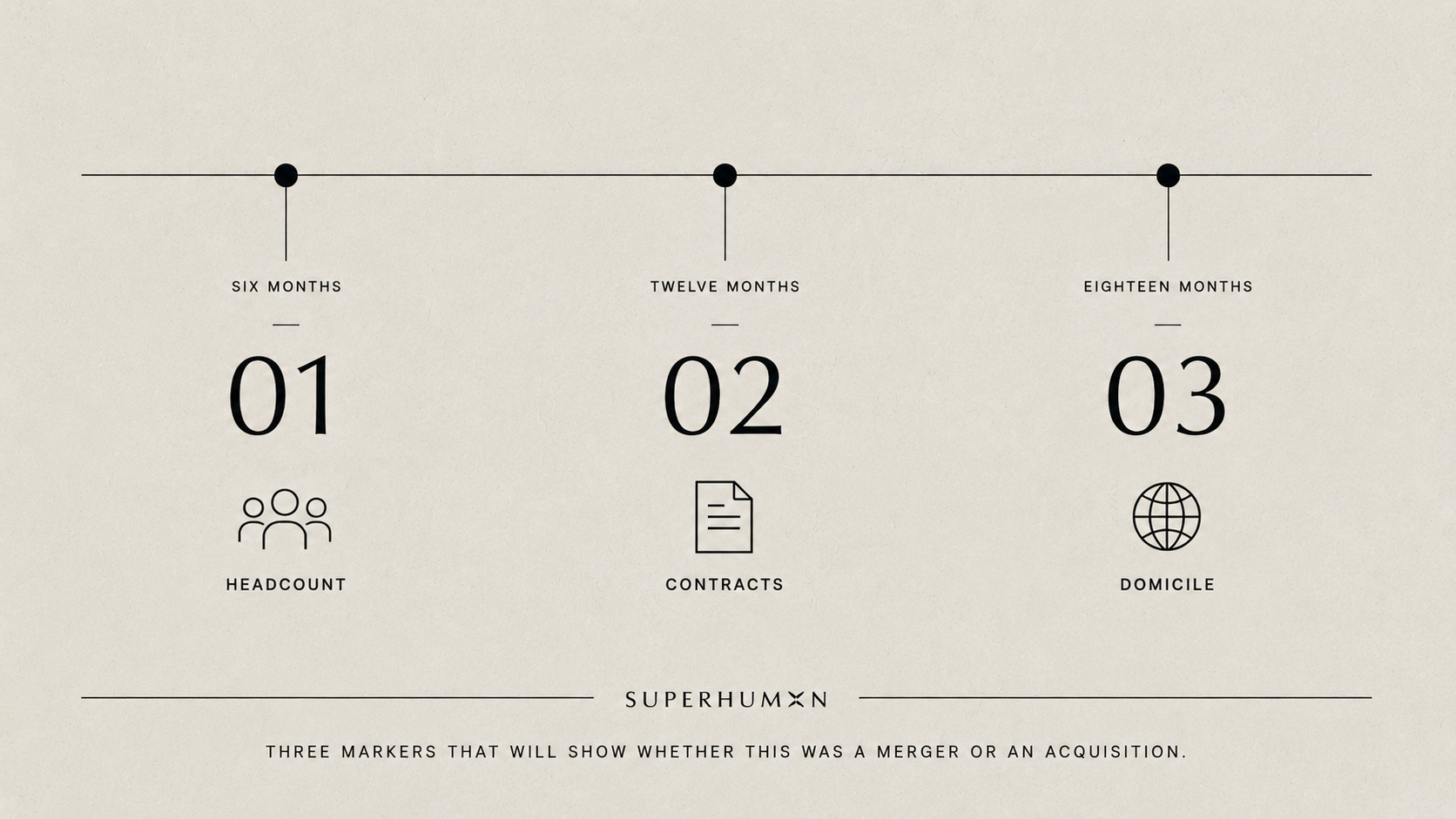

Markers

What to watch

Headcount is the first marker. An acquiring company integrating a smaller one typically consolidates overlapping functions within twelve to eighteen months. If Aleph Alpha's roughly 200 employees remain close to that number a year from now, in distinct roles, that would evidence the "anchored in Germany and Canada" claim. If headcount drops, particularly in non-engineering functions where overlap is highest, the ownership structure is doing what ownership structures tend to do.

Leadership composition is the second. Gomez declined at the announcement to specify who would make up the combined company's executive team. When that roster becomes public, the proportion of senior roles held by people from Aleph Alpha relative to Cohere will say more about how power is distributed than any number of press conference quotes.

The domicile question is the third. Gomez said only that Cohere would remain Canadian headquartered and owned, which is a carefully worded answer. It leaves open whether meaningful operational and legal control sits in Germany or whether Germany receives a European headquarters address while Toronto keeps the substance.

Customer retention is the fourth. Aleph Alpha's named enterprise customers chose a German vendor partly because of where that vendor was headquartered and regulated. If those contracts survive the transition to a Canadian-controlled parent without renegotiation, the sovereignty framing holds up for the customers who rely on it. If a share of those customers uses the ownership change to revisit their vendor relationship, the original pitch was tied to Aleph Alpha specifically rather than to the combined entity's new structure.

All four markers are verifiable within twelve months through public information, including regulatory filings, executive bios, customer case studies, and headcount tracking. None require inside access to deal terms.

Image created by the Superhumxn team.

Three markers that will indicate whether this was a true merger or an acquisition.

Next

Cross-border AI deals

Cohere and Aleph Alpha are unlikely to be the last AI companies from different countries to announce a deal in the language of partnership while structuring it as something else. The pattern, a national AI ambition on each side, a genuine technical justification sitting alongside a convenient political one, and an ownership structure disclosed in trade press rather than the joint statement, is likely to repeat as more countries push their AI companies to combine with foreign partners rather than be absorbed by American labs.

Check the ownership percentage before the adjectives. "Powerhouse," "anchored in," and "uniting" are narrative choices. The numbers that reveal what happened, headcount on each side, ownership split, who keeps the CEO title, who controls the domicile, are usually available within days in trade press and filings. The merger language tends to resolve into something more legible once you look at those first. Not necessarily wrong.

Diligence

For anyone doing diligence on cross-border AI consolidation, whether as an investor, an advisor, or someone trying to understand where European AI sovereignty claims are substantive versus rhetorical, the Cohere-Aleph Alpha deal is a useful template. The gap between language and structure is unusually well documented. Most acquisitions dressed as mergers don't get their ownership split reported by name within days of the announcement. This one did, and the 90/10 figure tells you almost everything the "powerhouse" language was built to obscure.

The deal may well work. Schwarz Group's infrastructure investment is real, the EU AI Act compliance need is real, and Cohere gains European market access and R&D talent it did not have before. The deal may well work. But the gap between what was announced and what was agreed tends to materialise with time. This will typically become evident in headcount figures and leadership changes, and usually after the initial coverage has moved on.